The New Car Market Q1 Update: Where Are We Now?

In this blog, we’re stripping back the jargon to break down what’s happened to the New Car market in Q1 and most importantly how you can use that info to sell more cars today. We’ll cover topics like…

An overall Q1 summary

Changing brand landscape

Price competition

The electrification of the market

Opportunities for retailers to win

If you’ve got the time, we went deep into all of this in our New Car Market Watch: Q1 Update webinar which you can watch here.

In a rush? No worries. We’ve also filmed a 10-minute video below that covers the absolute essentials.

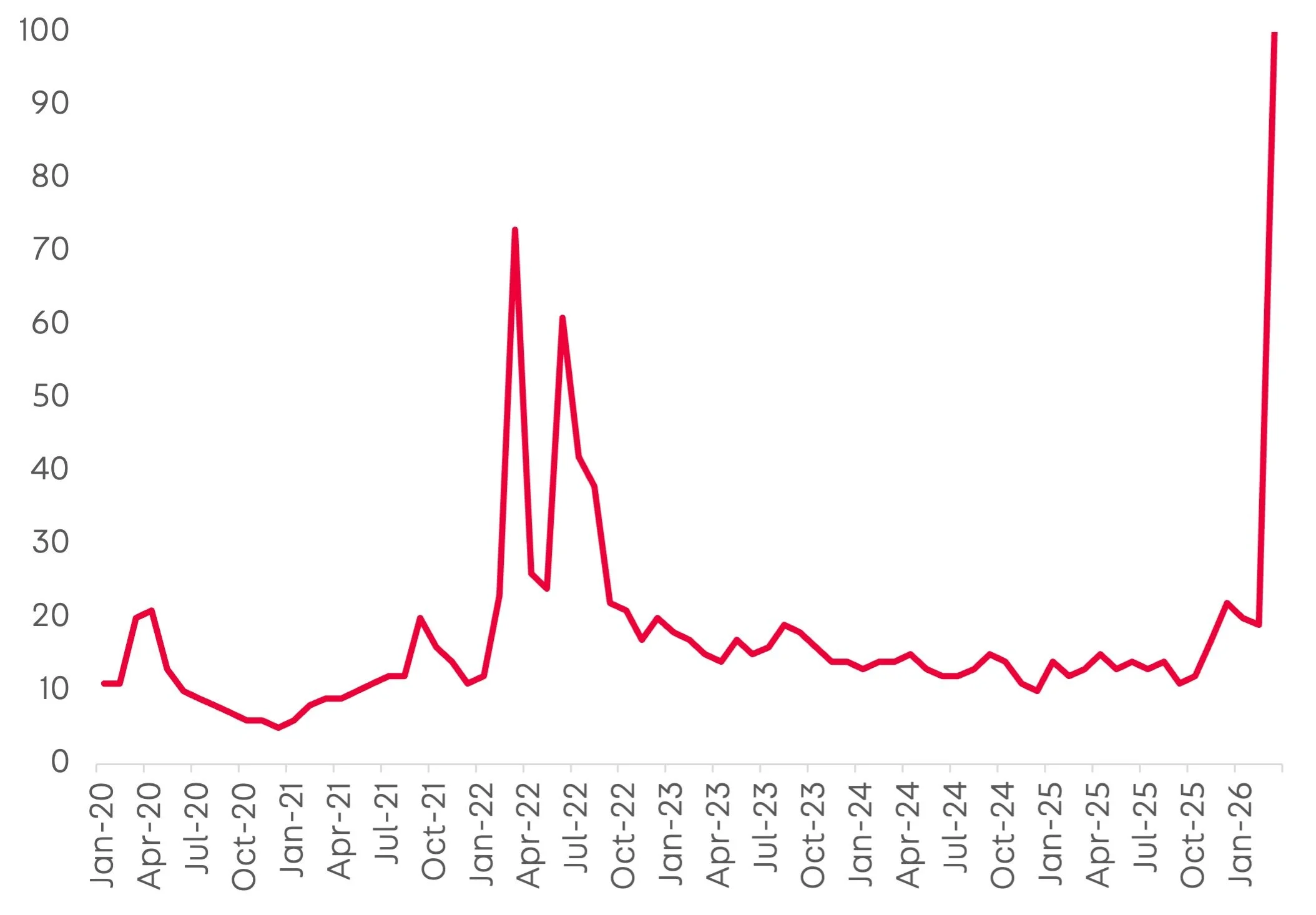

‘Petrol Prices’ UK Google Trends Index

Q1 wrap up

Q1 kicked off strong for the new car market with the best March and opening quarter since 2019. As we know, the first quarter sets the tone for the rest of the year, so this is a great start. New car sales are up +7% from March 2025 and Q1 was 6% ahead of Q1 2025¹. We also observed a +7% increase in the new car audience on Autotrader this quarter¹. Although we have seen growth, we cannot ignore the impact the US-Iran conflict has had on the market. As buyers become nervous about fuel shortages, we have seen this begin to impact their buying behaviour. There has been a record level of google searches for ‘petrol prices’ in the UK² as buyers begin to fear potential fuel shortages. This fuel anxiety has pushed buyers towards EVs, with an EV enquiry happening every single minute in March across new and used cars¹.

Geopolitical tensions, economic uncertainty, and rising fuel costs have influenced consumer confidence slightly but according to the GfK’s consumer confidence score, UK confidence is still similar to previous March months. The market has remained resilient, with 9-in-10 people on Autotrader saying that they’re more confident or just as confident in being able to buy their next car as they were last¹ and 73% of people saying they plan to buy in the next 6 months¹.

Changing brand landscape

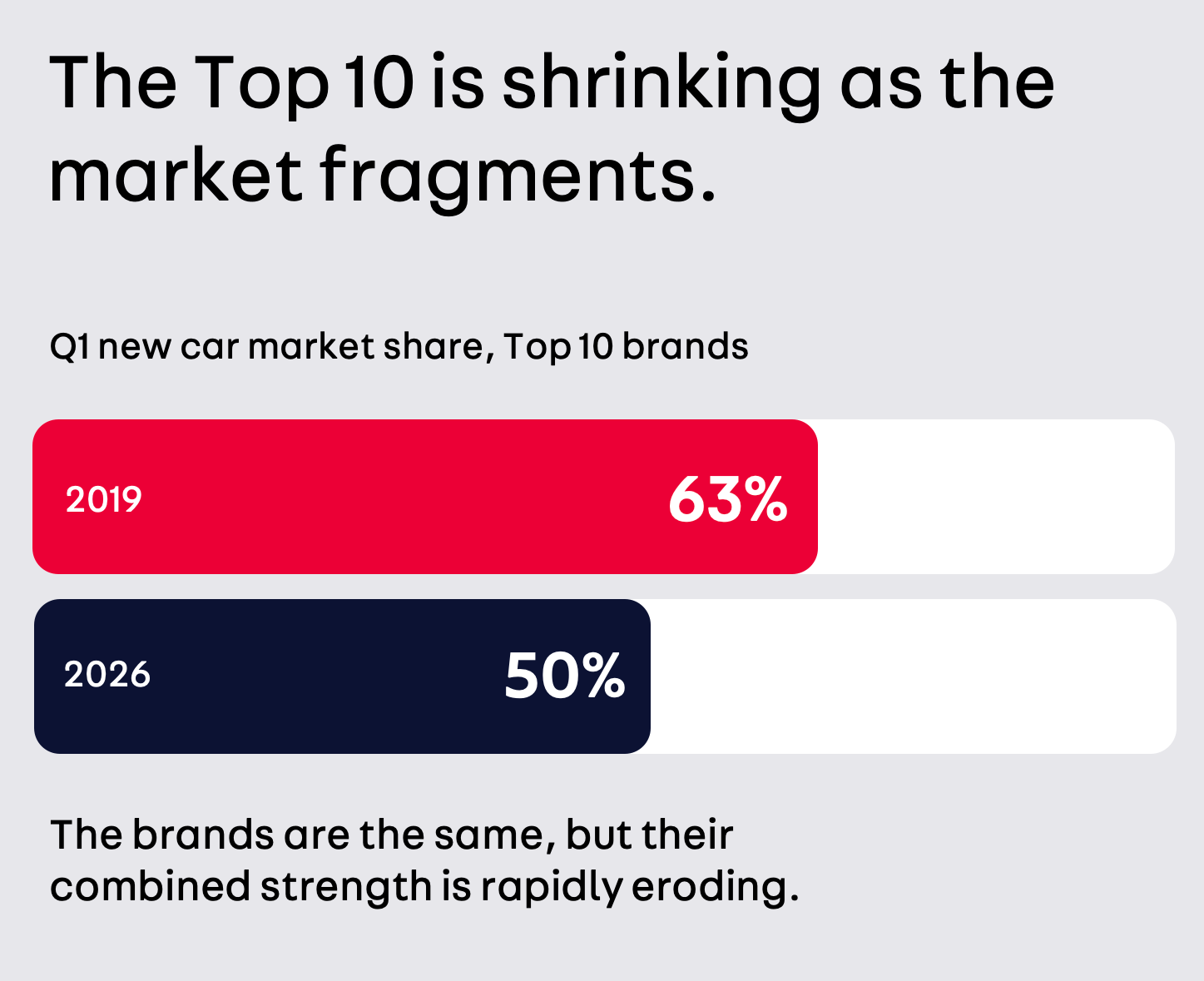

The brand landscape is changing before our very eyes. With the top 10 performing brands remaining unchanged, Volkswagen, Kia and BMW still holding the top three positions¹. However, the combined strength of the top 10 brands is rapidly eroding with 8/10 of these brands losing market share¹, and customer loyalty continuing to decline as EV adoption accelerates.

So where is that market share going?

Chinese brands are driving much of the disruption. In Q1, they accounted for half of the top 10 fastest growing brands and captured over 15% of new car sales¹. March also marked a milestone as thefirst time a Chinese car was the most sold model, the JAECOO 7¹.

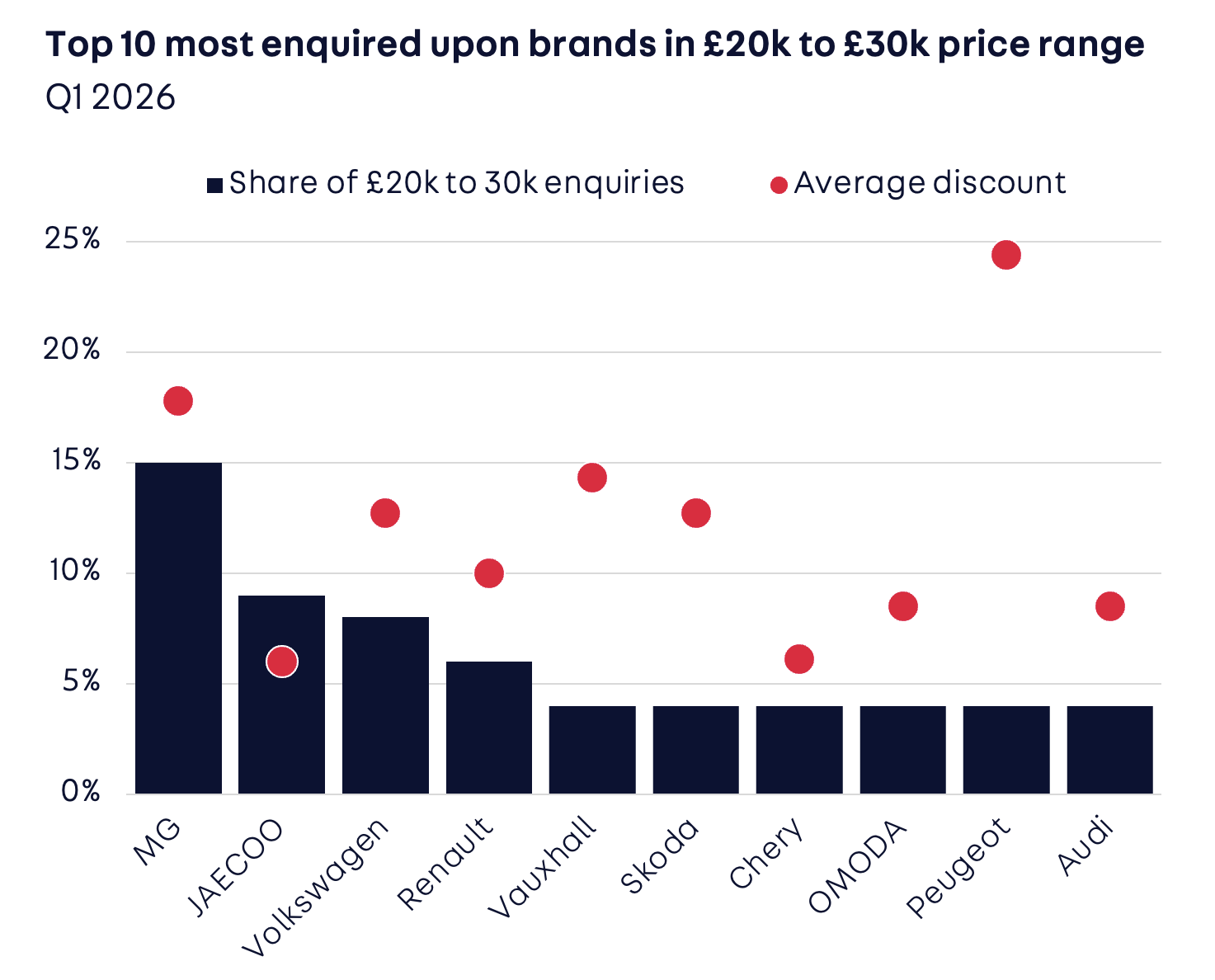

That said, the household names aren't out of the race. Established brands still generate the most enquiries on Autotrader with Land Rover, BMW, and Audi taking the top 3 spots¹. But the Chinese brands are gaining ground fast. They now hold four of the top 10 enquiry spots, with MG in 5th, JAECOO in 6th, BYD in 8th, and Chery in 9th¹.

All this together points to a market in transition. Legacy brands remain dominant for now, but their position is under increasing pressure. Chinese manufacturers are emerging as credible, high-growth competitors that are reshaping the competitive landscape.

Price competition

As new brands enter the UK market and fight for market share, pricing pressure has increased. This quarter, it’s all about the deals: a massive 80% of all new cars carried a discount, and + 40% came with a finance offer¹. March was particularly significant, accounting for 65% of private registrations and largely driven by record discounts¹. The average discount reached 10.9% with 5-in-6 brands increasing discounts YoY¹. The electric segment was by far the most competitive with average discounts rising to 12.8%¹.

This pricing competition is also reflected in monthly payments. The £300-£400 monthly payment pricing band accounts for 4-in-10 new car leads¹, while <£400pm took 2-in-3 enquiries on Autotrader¹. More affordable models, as a result captured a significant share of demand this quarter.

However, competitive pricing alone isn’t the only path to success. Brands are winning through implementing strategies such as clear pricing, strong monthly payment visibility and effective merchandising. For example, three of the most enquired about vehicles in Q1 were from Land Rover¹, a brand that we’ve seen perform successfully applying these principles

The electrification of the New Car Market

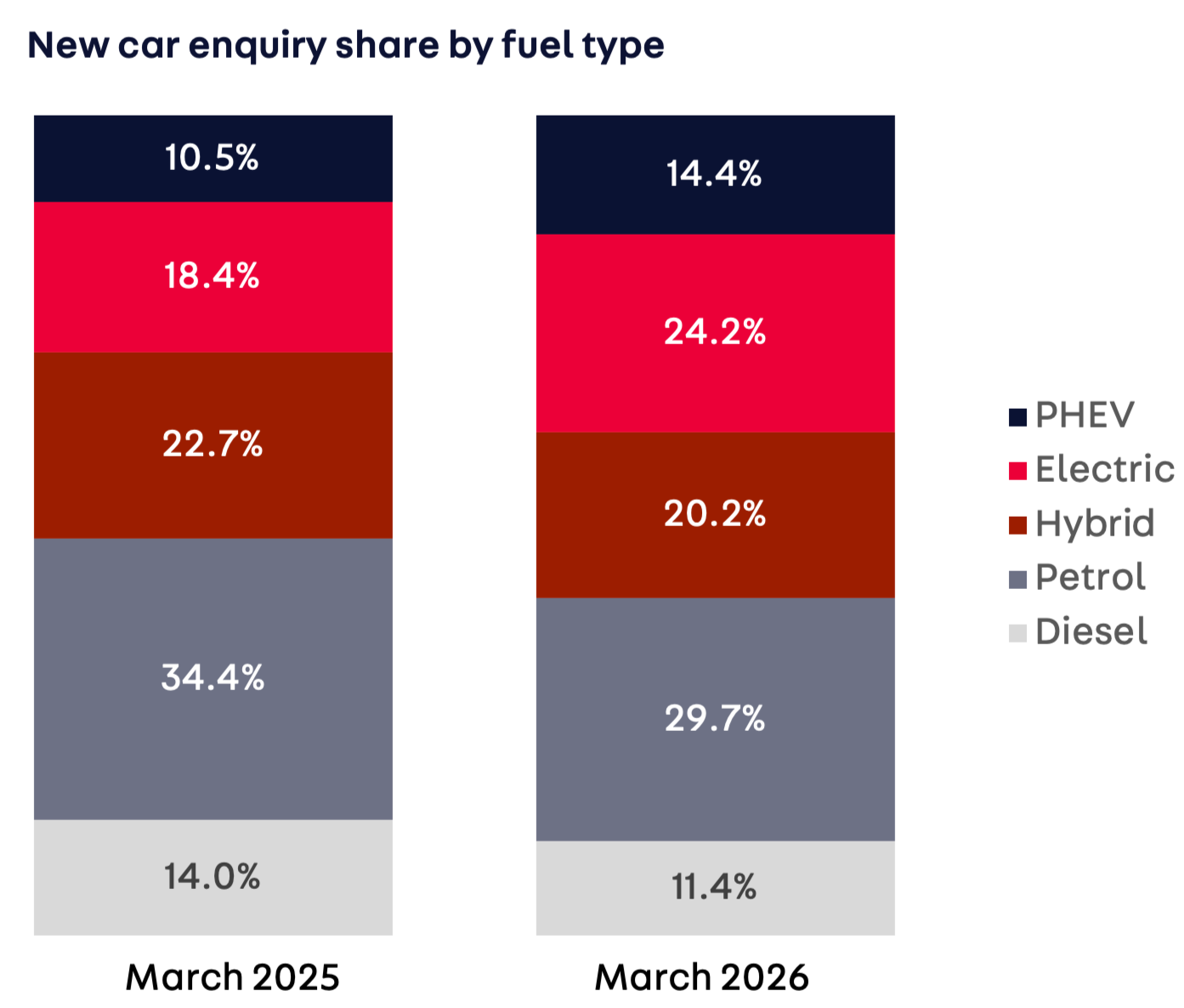

Retailers are currently navigating a complex "slow but steady" transition as the ZEV mandate target jumps to 33% of all new car registrations this year. While we saw a respectable 15% lift in BEV sales compared to Q1 2025¹, that growth hasn't quite kept pace with the rising regulatory bar, leaving a gap that dealers must now work to bridge. The good news is that consumer appetite is reaching a critical mass; in Q1, electrified options (BEVs, HEVs, and PHEVs) captured a majority 50.1% market share¹. This shift likely fuelled by rising petrol costs as in March we saw a surge in interest, with one-in-four new car enquiries being an EV. Alongside this, for the first time ever, the average advertised price for an EV actually dropped below petrol cars in March. That’s a massive win for retailers and a perfect way to win over anyone still sitting on the fence about the cost of switching.

Opportunity

To stay ahead of the curve, retailers must move beyond traditional reliance on brand loyalty and take decisive action on the showroom floor. Success in this evolving market hinges on understanding and beating the competition by stocking the specific models where demand is surging particularly in the electrified space and backing that inventory with targeted plans to drive awareness, consideration, and conversion. It is essential to maintain a rigorous retail process: ensure monthly payments are highly visible and easy to compare, and focus on the levers you can control, such as merchandising. As we’ve seen with brands like Jaecoo, success is possible through smart positioning without having to aggressively pull the discount lever. Now is the time to be bold on electric; with the ZEV push intensifying and fuel prices remaining volatile, the retailers who proactively lean into the EV transition will be the ones best positioned to capture the next generation of car buyers.

¹Autotrader Internal Data 2026

²UK Google Trends Index